Over 220 Chemical Companies Suspend Pricing: Titanium Dioxide Price Hike of $250/MT Signals Deepening Supply Tightness in the Global Chemical Industry

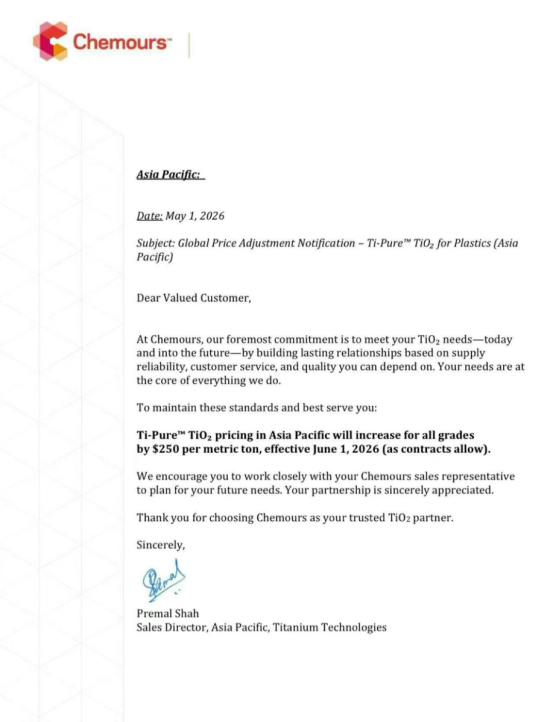

Recently, Chemours announced a new price adjustment: effective June 1, 2026, all grades of titanium dioxide in the Asia-Pacific region will increase by USD 250 per metric ton. This marks the third major price hike issued by Chemours in 2026, highlighting continued tightening in the global chemical supply chain.

Since the beginning of 2026, bulk chemical prices in China—including titanium dioxide—have continued to rise. The escalation of geopolitical tensions in February further accelerated raw material cost increases. Moving into April and May, the market has shifted beyond simple price inflation, entering a new phase characterized by widespread price suspensions and supply shortages.

Over 220 Chemical Companies Suspend Quotation Across the Entire Value Chain

On May 6, 2026, China’s chemical market experienced a peak in what industry participants are calling a “pricing freeze wave.” According to incomplete statistics, more than 220 chemical companies suspended quotations for over 100 products on the same day.

The suspension covers multiple segments of the chemical industry, including solvents, resins, additives, pigments, phosphate chemicals, and coal-based chemicals.

The main drivers include:

-

Scheduled plant maintenance and shutdowns

-

Prioritization of internal consumption over external sales

-

Low inventory levels

-

Volatile raw material pricing

-

Regional supply-demand imbalances

For downstream industries such as coatings, waterproofing, plastics, and construction materials, key inputs including epoxy resins, titanium dioxide, industrial solvents, bromine, and pentane series products have been widely affected, directly disrupting production planning and cost control.

Broad-Based Suspension Across Regions and Product Categories

The current wave of suspension is concentrated in major chemical production bases such as Shandong, Hebei, Anhui, Sichuan, Hubei, Liaoning, Shanxi, Guangdong, and Henan.

In the oil, gas, and refining sectors, multiple companies have suspended quotations for LNG, marine fuel oil, diesel, and asphalt. Many suppliers now operate on a “fixed customer supply only” model, with no open market pricing available.

Key chemical intermediates have also entered large-scale suspension:

-

MTBE has become one of the most severely affected products

-

Propylene and isobutylene plants are operating at low loads or have shut down

-

n-hexane, n-heptane, isohexane, and pentane foaming agents are widely unavailable

-

High-purity, low-sulfur products are only supplied to long-term contract customers

Coal-based and basic chemicals are also tightening significantly. Ammonia, methanol, sulfuric acid, hydrogen peroxide, and chloroform are increasingly diverted to internal use or controlled supply channels.

In phosphate chemicals, producers in Hubei, Sichuan, and Yunnan have largely suspended quotations for MAP and DAP, with trading shifting toward negotiated, order-based transactions.

136 Chemical Products Rose in April—The “Suspension Wave” Was Already Building

The current disruption did not emerge suddenly.

In April 2026 alone, 136 chemical products recorded price increases in China, with 57 items rising more than 5%. Despite already elevated price levels, the market continued its upward trajectory, further intensifying cost pressure across the supply chain.

Key raw materials in the coatings industry also rose sharply:

-

Titanium dioxide increased by 12.58%

-

Propylene increased by 8.08%

-

Alcohol ether and ester solvents continued to climb

-

Resin and related intermediates followed the same upward trend

These sustained increases have significantly raised production costs for coatings, specialty chemicals, and construction materials.

Downstream Industries Accelerate Price Pass-Through

Facing persistent raw material inflation, leading coatings and waterproofing companies have implemented multiple rounds of price increases.

-

Three Trees Co., Ltd. raised prices of interior/exterior coatings, waterproofing, and flooring systems by 3%–25% starting May 1

-

Orient Yuhong, Beixin Waterproofing, Keshun Co., Ltd., and Dayu Waterproofing collectively increased engineering waterproofing product prices by 3%–8%

-

Kairen Co., Ltd. also adjusted its waterproofing product prices upward

Meanwhile, small and medium-sized coating manufacturers have followed with additional price hikes and tighter payment terms, prioritizing cash-based and high-credit customers.

Internationally, beyond Chemours, Dow has also implemented multiple rounds of polyethylene price increases, with cumulative gains approaching 100%.

From “Price Increases” to “Supply Shortages”: Market Stress Expected to Continue

Industry observers note that the core challenge in the chemical sector has shifted from rising prices to outright supply shortages.

Many companies have stopped public quoting entirely, offering only contract-based supply to existing customers. As maintenance shutdowns increase in late May and June, further delivery delays and supply constraints are expected.

For downstream sectors including coatings, waterproofing, plastics, and construction materials, the industry is entering a high-cost, low-inventory cycle with continued volatility in both pricing and availability.

| Enter Zhuocheng | Product | Honorary Qualifications | Contact Us |

| Company IntroductionFactory Appearance | Raw materials Premixed agent product OEM products |

Company:Jinan Zhuocheng Bio-Tech Co., Ltd. Corporate email:info@zhuochengbio.com Address:Building 3, Ligao International, 1222 West Aoti Road, Lixia District, Jinan |